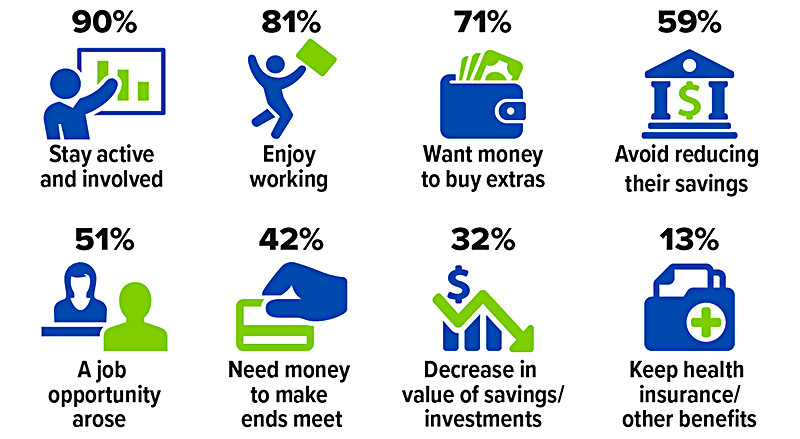

Are you hoping to travel the world after you retire? Traveling is the most common activity people dream of doing after they stop working (65%, according to a November 2021 Transamerica Center for Retirement Studies survey)—and it’s totally possible for most retirees. With a bit of planning, creativity, and discipline, you’ll be ready to jump on your transportation of choice and experience unforgettable moments. The following tips will help you turn that daydream into your retirement reality.

KEY TAKEAWAYS

- Travel is the most popular dream of retirees, with 65% expressing a wish to see the world.

- Before you just set off, be honest with yourself about your love of being on the road, your obligations to others, and the state of your health.

- Traveling can be expensive, so look carefully at your retirement savings and make sure that the cost of traveling is incorporated into your retirement plan.

- Medicare generally doesn’t cover your healthcare costs outside of the United States and its territories, so additional healthcare insurance may be necessary.

Make a Plan Before Retirement

Retirement planning is an ongoing, multistep process. If you already know travel is on your retirement bucket list, you should factor the cost into your plans. To ensure a comfortable, secure, and fun retirement, you’ll want a personalized plan based on the following:

- Retirement date

- Financial and investment goals

- Risk tolerance

- Retirement lifestyle

To help solidify your plans for traveling during retirement, consider doing these things.

- Discuss your travel ideas: Where do you want to go? What type of traveler are you? Do you plan to take short trips, or will you go the nomad route of retiring with no permanent home? Be specific and realistic, as costs will vary greatly.

- Consider your finances: Based on your anticipated retirement income, what type of travel will you be able to afford? The U.S. Department of Labor has a set of interactive worksheets, such as a balance sheet, to help you organize all your accounts and calculate your net worth.

- Plan for Social Security benefits: Social Security is a major income source for many retirees, and the age at which you begin claiming benefits affects how much you will receive. Plan your ideal age to start receiving benefits using this claiming age calculator. You can also get an estimate of your future benefit by checking your Social Security account.

- Factor in health concerns: Do you or your partner have any health issues that may impact where and how you can travel?

- Make a list of wants and needs: What kind of amenities, culture, access to healthcare and public transportation, etc. are you looking for? What is nice to have and what is non-negotiable?

Planning for the above will help you create a realistic retirement plan that includes travel. See if you have access to retirement planning and savings tracking tools through your 401(k) or individual retirement account (IRA). You can also talk with a financial advisor.

Create a Retirement Travel Budget

If you’re like most retirees, a retirement travel budget will be key to making sure you can afford everything you want to see and do. According to Fidelity, most retirees will spend between 55% and 80% of their annual working income each year in retirement. If you plan to travel frequently in retirement, you’ll need to raise that percentage. For reference, the average retiree spends $11,077 per year on travel.

To begin building a retirement travel budget that matches your situation, estimate your future travel expenses. Research cost of living, accommodations, groceries, eating out, and other activities in the places you want to visit to get a rough idea of your future spending needs. The U.S. Department of Labor’s planning worksheets include a “Goals & Priorities” section to help you prioritize what you save based on short- and long-term goals. Then use the “Cash Flow Spending Plan” worksheet to build a guide for how you expect to spend your money. Track actual spending to compare it with what you planned.

Use the 50/30/20 Spending Rule to Budget for Travel in Retirement

Kimberly L. Curtis, a certified financial planner (CFP) at Wealth Legacy Institute, recommends the 50/30/20 rule to budget for traveling in retirement. This budgeting framework breaks after-tax income into three main categories with corresponding percentages.

- Needs (50%)

- Wants (30%)

- Savings (20%)

Based on this rule, cash flow for spending on travel in retirement comes out of the 30% allotted for wants.

“Retirees spend, on average, 5% to 10% of their annual budget on travel,” Curtis said. “Instead of a monthly dollar amount, many retirees will ‘chunk’ their retirement travel budget into annual amounts. For example, a big European trip might mean putting aside $10,000 for that year. Otherwise, retirees may plan on around $5,000 a year for the next 10 to 15 years of retirement.”

Consider Insurance

Retired travelers’ needs may differ from those of younger travelers, particularly the potential need for medical care while on the road. Individuals become eligible for Medicare at age 65. If you plan to travel during retirement, make sure you don’t miss your initial enrollment period.

Medicare Parts A and B cover hospital care and doctor visits in all 50 U.S. states, the District of Columbia, and all U.S. territories (Puerto Rico, the U.S. Virgin Islands, Guam, American Samoa, and the Northern Mariana Islands) as long as the provider accepts Medicare.8 Certain Medicare Advantage (MA) plans also provide state-to-state coverage, including a national pharmacy network.

Keep in mind that many MA plans limit the amount of time you can spend outside your service area (i.e. your state) and still be covered (for example, six months).8 Additionally, once you travel outside the U.S. Medicare generally doesn’t cover healthcare.9 For this reason additional insurance is recommended for traveling during retirement.

If you want to travel the world after you retire, consider additional travel insurance to protect against potential medical emergencies. Travel insurance may also cover inconveniences such as trip cancellations or interruptions and lost or stolen baggage.

What to Consider When Selecting Travel Insurance

Cost shouldn’t be the only factor when choosing travel insurance. Travel expert Chris Appleford of Travelling Apples notes some of the most important coverage options to look out for:

- Medical coverage (including medical expenses, evacuation, and repatriation in case you need to be brought back to the U.S. for care)

- Trip cancellation or interruption

- Travel delays

- Luggage and personal belongings

- Terms and conditions surrounding pre-existing conditions

- Coverage duration

How to Cut Down on Travel Costs

Balancing cash flow can get tricky when you’re no longer receiving a paycheck or business income. Cutting down on travel expenses is one of the biggest concerns for retirees as they explore the world.

Hotel, airline, and attraction prices are highest in summer and on weekends, so retirees with flexible schedules can save money by traveling in the offseason. The same flexibility can pay off when it comes to travel dates and destinations. Kasper de Wijs, travel expert and owner of HotelRoutePlanner.com, says travel websites and newsletters often post destination-based deals and last-minute offers.

De Wijs also recommends exploring senior discounts, early bird discounts, and loyalty programs for travel-related services. Amber Dixon of Elderly Guides agrees that most establishments offer discounts to seniors. She adds that house swapping with other travelers or making house sitting arrangements can also save retirees on accommodation costs. Sites such as Trusted Housesitters and Mind My House.com connect home owners and house/pet sitters with each other.

Explore the Open Road to Save Money on Travel in Retirement

For slightly more adventurous, lower-cost travel, many retirees swear by recreational vehicle (RV) camping. The purchase of an RV is an up-front cost, for sure, but as many RV travelers live in their vehicle for months at a time, other costs are absorbed or reduced. For example, you’re eating most meals in, and the site fee is small compared with hotels or Airbnbs.

Andrew Kuttow, RV enthusiast and travel blogger at RVCampGear.com, notes that memberships with organizations such as Good Sam, AAA, and AARP often include camping and travel discounts.

“You might also consider an America the Beautiful Senior Pass,” Kuttow said. For $80, a lifetime senior pass allows access to more than 2,000 recreation sites managed by the National Parks Service and other federal agencies. An annual Senior Pass is $20. You must be 62 years old to be eligible.

What Percentage of Older People Travel?

According to the AARP Travel Trends survey, 62% of people age 50 and older plan to take at least one leisure trip in 2023, with the majority taking between three and four trips. However, those who are 70 and older plan to spend 40% less on travel in 2023 than they did in 2022. They are also the group most cautious about COVID-19.

How Much Do I Need in Retirement to Travel?

It depends on your retirement plan, overhead costs, and budget. Kimberly L. Curtis, a CFP at Wealth Legacy Institute, says that retirees pay between 5% and 10% of their annual budget on travel and puts the average yearly amount at about $5,000 for the first 10 to 15 years of retirement. AARP’s 2023 Travel Trends survey found that people 50 and over planned to spend an average of $6,688 on travel in 2023.

What Is the Cheapest Way to Travel in Retirement?

There is no one answer to this question, but there a number of ways to curtail the costs of travel, including traveling in the off season, having flexibility re dates and destinations, and taking advantage of senior discounts, early bird discounts, and loyalty programs. There are also house swapping and house sitting arrangements. The adventurous can buy an RV and travel the open road, saving on restaurant costs (by eating in) and accommodation costs (by sleeping in).

The Bottom Line

Traveling is a popular pastime for many people, and retirees are no exception, especially with all the free time they have on their hands. However, if you want to travel in retirement, and particularly if you want to travel internationally, it takes prudent planning starting early in your professional career. You need to decide how and where you want to travel, then build those costs into the total amount you are saving for retirement. Don’t forget to factor in healthcare concerns and when you should start taking Social Security. There are also plenty of cost-cutting measures you can take to make your journeys more affordable.